- mzmauto

How Does a Car Leasing Agreement Work for First-Time Drivers?

Quick Answer: A car leasing agreement allows a first-time driver to use a vehicle for a fixed period, usually 24 to 36 months, by paying for its expected depreciation rather than buying it outright. You do not own the vehicle. Instead, you agree to mileage limits, insurance requirements, and monthly payments under a legally binding contract. For first-time drivers, approval depends primarily on:

Unlike financing, lease payments do not build equity. At the end of the term, the vehicle is returned, purchased at a predetermined residual value, or replaced with a new lease. Did You Know? Many first-time applicants are surprised to learn that lenders evaluate credit stability more heavily than driving experience when approving a lease. Leasing can offer lower monthly payments than buying, but it also introduces contract restrictions that beginners must fully understand before signing. |

For many first-time drivers, the biggest question is not just “How do I get a car?” but “Can I even qualify for one without years of credit history?”

A car leasing agreement can seem like an easier entry point because monthly payments are often lower than financing. But approval is not automatic. Lenders evaluate credit stability, income consistency, and insurance eligibility, not just whether you’re a new driver.

At the same time, first-time applicants face unique challenges: limited credit history, higher insurance premiums, and uncertainty about long-term driving needs. Choosing a lease without understanding the structure can create financial strain just as easily as it can provide flexibility.

Before signing anything, it’s important to understand how leasing works, specifically for beginners, from qualification requirements to contract obligations and long-term cost impact.

Can First-Time Drivers Qualify for a Car Leasing Agreement?

Many first-time drivers assume leasing is easier than financing. In reality, leasing often requires stronger credit stability because the vehicle remains the lender’s asset throughout the contract. Approval is based less on driving history and more on financial reliability.

Understanding what lenders evaluate helps beginners realistically assess their chances.

Credit Score Requirements

Most leasing companies prefer applicants with credit scores in the 680+ range, though approvals can occur below that threshold depending on income strength and lender flexibility.

- Higher credit scores qualify for lower money factors (better financing terms)

- Limited credit history can trigger higher rates or require a cosigner

- Subprime approvals are possible but typically more expensive

Did You Know? Leasing companies often use tiered credit systems. Moving up just one credit tier can significantly reduce your money factor and total lease cost.

For first-time drivers with “thin” credit files, the challenge is not necessarily low credit; it’s limited credit history.

Income and Debt-to-Income Ratio

Lenders evaluate whether your income can comfortably support the monthly lease payment.

- Stable employment history strengthens approval chances

- Many lenders prefer total vehicle expenses to remain under 15–20% of monthly gross income

- Debt-to-income (DTI) ratios typically should stay below 40–45%

Note: Even with a solid credit score, high existing debt can reduce the likelihood of approval.

The Role of a Cosigner

A cosigner can significantly improve approval odds for first-time drivers with limited credit.

- The cosigner agrees to assume legal responsibility if payments are missed

- Strong cosigner credit can reduce the money factor

- The lease appears on both credit reports

Important Insight: Missed payments affect both the driver’s and the cosigner’s credit scores.

Insurance Considerations for First-Time Drivers

Insurance is mandatory for leased vehicles and typically requires:

- Liability coverage

- Collision coverage

- Comprehensive coverage

Young or first-time drivers often face higher premiums.

Data Insight: Drivers under 25 can pay 50–100% more for insurance than drivers in their 30s, depending on the state and driving record. This cost must be factored into lease affordability calculations.

Approval Reality Check

For first-time drivers, leasing is possible, but not guaranteed. Approval strength depends on:

- Credit stability

- Income verification

- Manageable debt levels

- Insurance affordability

Leasing companies are primarily assessing financial risk, not driving experience. Preparing these financial components in advance increases approval probability and improves lease terms.

Next, we’ll walk you through the leasing process step by step, from budgeting to contract signing.

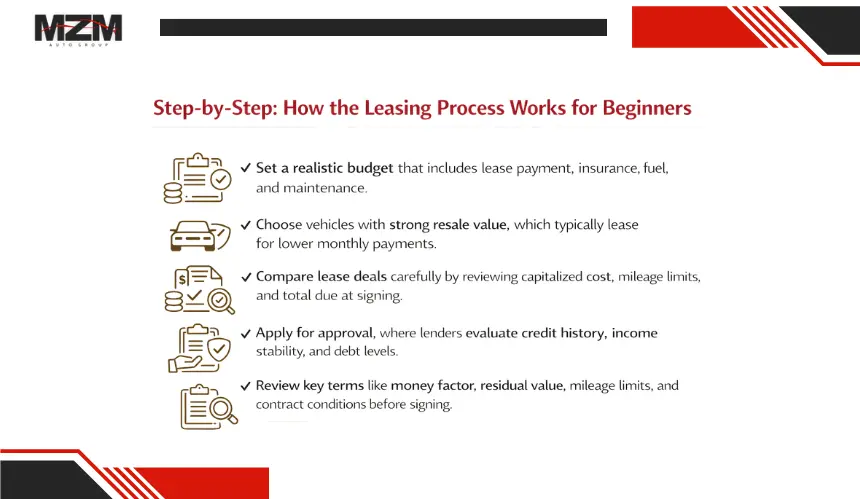

Step-by-Step: How the Leasing Process Works for Beginners

For first-time drivers, the leasing process feels simple at the dealership, but the approval and pricing decisions are driven by finance terms that are easy to miss. The goal is to control the total cost, not just “get approved.” Here’s how the process typically works from start to finish.

Step 1: Set a budget

Before shopping, the budget should be based on the total monthly vehicle cost, not just the lease payment. For first-time drivers, insurance can be the swing factor that makes an “affordable” lease unaffordable. A realistic budget accounts for the lease payment, insurance, fuel, and routine maintenance, then checks whether those combined costs still fit comfortably within income.

Note: Many lenders informally assess affordability using payment-to-income and debt-to-income ratios, so stable income matters as much as credit score.

Step 2: Choose the right vehicle type

Vehicle choice affects everything: lease pricing, insurance rates, and approval odds. Cars that hold value well tend to lease more favorably because depreciation is lower. On the other hand, higher-priced trims can quickly raise both monthly payments and insurance premiums, especially for new drivers.

Did You Know? Lease pricing is heavily influenced by the vehicle’s projected resale value. Higher residual value often means a lower lease payment because less depreciation is being financed.

Step 3: Compare lease deals the right way

Comparing leases is about understanding the structure, not chasing the lowest advertised monthly number. Two deals with the same monthly payment can have very different total costs depending on what’s due at signing, the mileage allowance, and the money factor.

A useful comparison checks the negotiated vehicle price (capitalized cost), the lease term, the mileage limit, and the total due at signing. This prevents the common mistake of choosing a “cheap payment” deal that simply pushes costs upfront.

Tip: If a lease payment looks unusually low, it may include a large down payment, a low mileage allowance, or a promotional incentive that only applies to certain credit tiers.

Step 4: Apply for approval

Once a vehicle and structure are selected, the dealership submits the application to the leasing company. Approval is largely based on credit stability, income verification, and existing debt obligations. First-time drivers with limited credit history may still qualify, but many will need a cosigner to access better terms.

Note: Leasing can be stricter than financing in some cases because the lender is forecasting the vehicle’s value years into the future and wants strong repayment reliability.

Step 5: Understand key leasing terms before signing

This is the most important step for first-time drivers because the contract terms determine the true cost. The capitalized cost is the negotiated price. The residual value is the predicted value at lease end. The money factor is the financing charge. Mileage allowance and wear standards control the potential penalties upon return.

Did You Know? A quick way to estimate the interest equivalent of a money factor is to multiply it by 2,400. This helps first-time drivers compare a lease’s financing cost with an auto loan APR.

Step 6: Confirm insurance requirements

Leased vehicles typically require full coverage, meaning liability, collision, and comprehensive insurance. Some leases also require gap coverage to protect against total-loss scenarios in which the car’s value is lower than the remaining payoff. For first-time drivers, insurance costs can be materially higher than expected, so this step should happen before final signing.

Step 7: Sign, pay initial fees, and take delivery

At signing, the first month’s payment is usually due along with registration fees and lender charges such as the acquisition fee. After paperwork is complete and insurance is verified, the lease becomes active, and the vehicle is delivered. From that point, the driver’s main obligation is to stay within mileage limits, maintain the vehicle properly, and make payments on schedule.

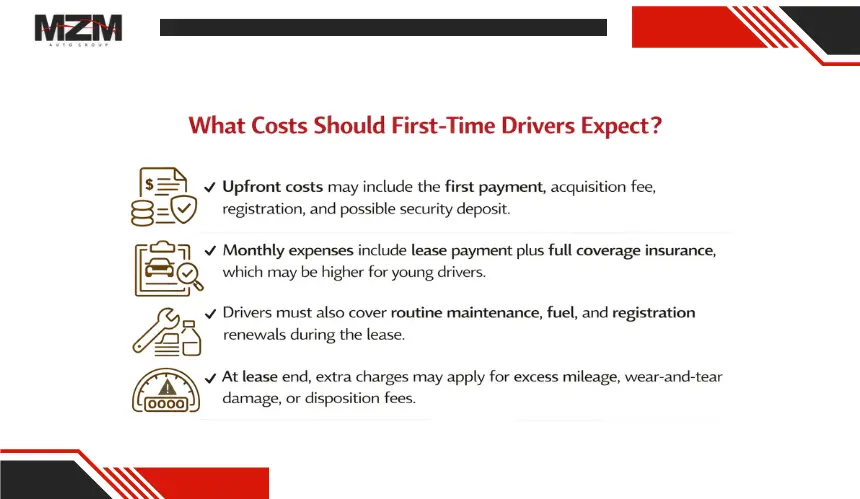

What Costs Should First-Time Drivers Expect?

Understanding the full cost structure of a car leasing agreement is especially important for first-time drivers. The monthly payment is only one part of the financial commitment. Insurance, upfront fees, and end-of-lease charges can significantly affect the total cost.

For beginners, overlooking these variables is one of the most common financial mistakes.

Upfront Costs

At signing, most leases require several initial payments. These typically include the first month’s payment, an acquisition fee charged by the leasing company, registration fees, and sometimes a security deposit. Some promotions advertise “low down payment” leases, but it’s important to examine how much is due at signing versus how the payment is structured over time.

Did You Know? Large upfront payments reduce monthly payments but do not build equity. If the vehicle is totaled early in the lease, insurance may not fully recover that upfront cash.

Monthly Financial Obligations

The recurring lease payment is based on depreciation and the money factor, but that is not the only monthly expense. First-time drivers must also carry full coverage insurance, which often costs significantly more for younger drivers or those with limited driving history.

Insurance can sometimes equal or even exceed the lease payment for high-risk age groups. This is why budgeting must include the combined total of payment plus insurance, not just the advertised lease amount.

Maintenance and Operating Costs

Although most leases remain within the manufacturer’s warranty period, routine maintenance such as oil changes, tire replacement, and brake servicing remains the driver’s responsibility. Fuel costs and registration renewals also continue throughout the lease term.

Because first-time drivers often select newer vehicles, warranty coverage reduces exposure to major repair bills, but it does not eliminate ongoing maintenance expenses.

End-of-Lease Costs

At the end of the lease, additional charges may apply. These can include excess mileage fees if annual limits were exceeded, wear-and-tear charges for damage beyond normal use, and a disposition fee for returning the vehicle.

Important Insight: Excess mileage charges typically range from $0.15 to $0.30 per mile. Driving just 4,000 miles over the limit could result in hundreds of dollars in added costs.

For first-time drivers, the key is understanding that leasing is a structured financial commitment with beginning, middle, and end costs. Evaluating the full lifecycle expense prevents overcommitting based on a low monthly payment alone.

Leasing vs Buying for First-Time Drivers

For beginners, the comparison becomes clearer when structured side-by-side. The financial mechanics, flexibility, and long-term impact differ significantly between the two models.

Comparison Factor | Leasing | Buying |

Monthly Payment | Typically lower because you finance depreciation only | Typically higher because you finance the full vehicle price plus interest |

Upfront Costs | Often lower, but may include acquisition fees and security deposit | Down payment varies; may require larger upfront cash |

Credit Impact | Builds credit with on-time payments; strict approval standards | Builds credit through installment loan repayment |

Ownership | No ownership unless the lease buyout is exercised | Full ownership once the loan is paid off |

Equity Building | No equity accumulation during the lease term | Payments reduce principal and build equity over time |

Mileage Flexibility | Annual mileage limits (10,000–15,000 typical) | No mileage restrictions |

Insurance Requirements | Full coverage required; often higher premiums for young drivers | Full coverage required if financed; optional after loan payoff |

Long-Term Cost | Continuous payment cycles if leasing repeatedly | Lower average annual cost after loan payoff |

Risk Exposure | Limited depreciation risk (within contract terms) | Full exposure to resale market fluctuations |

Flexibility | Easier to upgrade every few years | Better for long-term ownership stability |

Did You Know? Payment history makes up roughly 35% of common credit scoring models. Whether leasing or buying, consistent, on-time payments strengthen a first-time driver’s credit profile.

For first-time drivers, the right choice depends on income stability, projected mileage, insurance affordability, and long-term financial planning.

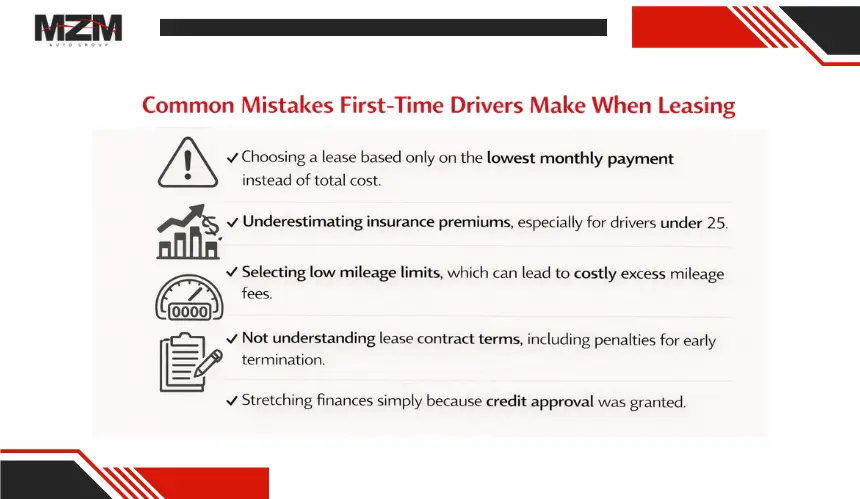

Common Mistakes First-Time Drivers Make When Leasing

For first-time drivers, the leasing structure can appear straightforward on the surface. But many financial pitfalls occur because beginners focus on approval rather than long-term cost clarity. Avoiding these mistakes can prevent unexpected expenses and contract stress.

Focusing Only on the Monthly Payment

The most common mistake is choosing a lease based solely on the advertised monthly payment. A low payment can sometimes hide higher upfront costs, a shorter mileage allowance, or a higher money factor.

Important Note: Two leases with identical monthly payments can differ significantly in total cost depending on term length and amount due at signing.

Underestimating Insurance Costs

First-time drivers, especially those under 25, often face higher insurance premiums. In some cases, insurance can equal or even exceed the lease payment.

Did You Know? Young drivers may pay 50–100% more in premiums compared to drivers in their 30s, depending on driving history and location.

Failing to factor insurance into total affordability can quickly turn a manageable lease into a financial strain.

Choosing Too Low a Mileage Allowance

Selecting a 10,000-mile annual allowance may slightly reduce the monthly payment, but exceeding it can result in penalties at lease end.

Excess mileage charges typically range between $0.15 and $0.30 per mile. Even moderate overages can add several hundred dollars to final costs.

Not Understanding Lease Termination Rules

Life changes, such as job relocation or income shifts, can make early lease termination tempting. However, lease contracts are structured around fixed depreciation schedules.

Ending a lease early can involve paying outstanding obligations, penalties, or negative equity.

Overcommitting Based on Credit Approval

Approval does not automatically mean affordability. Lenders evaluate credit risk, not personal budgeting comfort.

Tip: Even if approved, ensure the full vehicle cost, including insurance and operating expenses, fits comfortably within income rather than stretching to the maximum approval amount.

Is Leasing a Smart Choice for First-Time Drivers?

Leasing can be a practical entry point into vehicle access, but it is not automatically the best option for every beginner. The decision depends on financial stability, driving patterns, and long-term goals rather than simply qualifying for approval.

When Leasing Makes Sense

Leasing may be a strong fit for first-time drivers who have predictable income, moderate mileage, and a preference for newer vehicles under warranty.

- Stable employment with consistent monthly income

- Annual mileage within typical lease limits (10,000–15,000 miles)

- Access to a cosigner if credit history is limited

- Desire for lower monthly payments and shorter commitment cycles

Leasing can also reduce exposure to major repair costs because most leases end before the warranty expires.

Did You Know? Many lease contracts are structured around the period when vehicles experience the steepest depreciation but lowest repair frequency, typically the first 3 years.

When Buying May Be the Safer Option

Buying may be more appropriate for first-time drivers who plan to keep the vehicle long term or expect higher annual mileage.

- Driving more than 15,000 miles per year

- Intending to keep the vehicle beyond 5–7 years

- Prioritizing equity building and long-term cost efficiency

- Wanting freedom from mileage and wear restrictions

Ownership becomes financially stronger once the loan is paid off, because the vehicle can be used without ongoing monthly payments.

The Strategic Perspective

Leasing optimizes short-term affordability and flexibility. Buying optimizes long-term financial stability and asset retention.

For first-time drivers, the smarter option is the one aligned with realistic income, insurance affordability, and how long the vehicle will truly be kept, not simply the option that appears cheapest upfront.

Frequently Asked Questions

What credit score does a first-time driver need to lease a car?

Most leasing companies prefer a credit score of around 680 or higher, but approvals can occur below that depending on income strength and lender flexibility. Applicants with limited credit history may qualify with a cosigner. Higher credit tiers typically receive lower money factors and better overall lease pricing.

Can you lease a car with no credit history?

Leasing with no credit history is possible, but it is more challenging. Lenders may require a cosigner with strong credit or proof of stable income. Some captive finance companies offer first-time buyer programs, but terms may vary based on risk assessment.

Is leasing better than financing for students?

Leasing can provide lower monthly payments, which may help students manage short-term budgets. However, strict mileage limits and contract obligations can create risk if income or driving needs change. Financing may offer more long-term flexibility if the vehicle will be kept beyond graduation.

How much is typically due at signing for a first-time lease?

Upfront costs often include the first month’s payment, acquisition fee, registration fees, and possibly a security deposit. While some promotions advertise low amounts due at signing, total initial costs can still range from several hundred to a few thousand dollars, depending on the vehicle and credit profile.

Does leasing help build credit?

Yes. On-time lease payments are reported to credit bureaus and can help establish or strengthen credit history. Payment consistency matters more than whether the agreement is a lease or a loan. Missed payments, however, negatively affect credit just as they would with financing.

Can a first-time driver buy the car at the end of the lease?

Most car leasing agreements include a purchase option at a predetermined residual value. If the vehicle’s market value exceeds the residual value, exercising the buyout may offer a financial advantage. If it is lower, returning the vehicle may be the better decision.