- mzmauto

What Is Car Leasing and How Does It Differ From Buying a Vehicle?

Quick Answer: Most drivers focus on the monthly payment. Car leasing is a structured agreement where you pay for a vehicle’s depreciation over a fixed term, typically 24 to 48 months, without gaining ownership. At the end of the lease, you return the vehicle, purchase it at a predetermined residual value, or transition into another lease. Buying a vehicle, whether with cash or an auto loan, means you assume full ownership. Your payments build equity, the vehicle title transfers to you (or your lender during financing), and once the loan is paid off, you own the asset outright. The core distinction is simple but powerful:

According to industry data, new vehicles can lose 20–30% of their value in the first year alone, which is why lease payments are structured around predicted depreciation rather than total vehicle cost. That single financial mechanic explains most of the cost difference between the two options. Choosing between them is less about “which is cheaper” and more about time horizon, mileage habits, financial strategy, and risk tolerance. |

In Burbank, driving habits look different from those in many other cities. Daily commutes often mean navigating the 5 Freeway, studio corridors near Warner Bros., and steady traffic flowing toward Downtown Los Angeles. Add higher vehicle prices across Southern California and rising insurance costs, and the decision between leasing and buying becomes more strategic than it first appears.

California also has distinct financial variables that influence this choice. State sales tax applies differently to leased versus purchased vehicles, fuel costs are consistently among the highest in the country, and drivers in media, production, and freelance industries often prefer flexible vehicle cycles. At the same time, long-term residents who commute heavily may exceed standard lease mileage caps of 10,000–15,000 miles per year.

Next, let’s break down exactly how a lease agreement works, including the financial mechanics that shape those monthly payments.

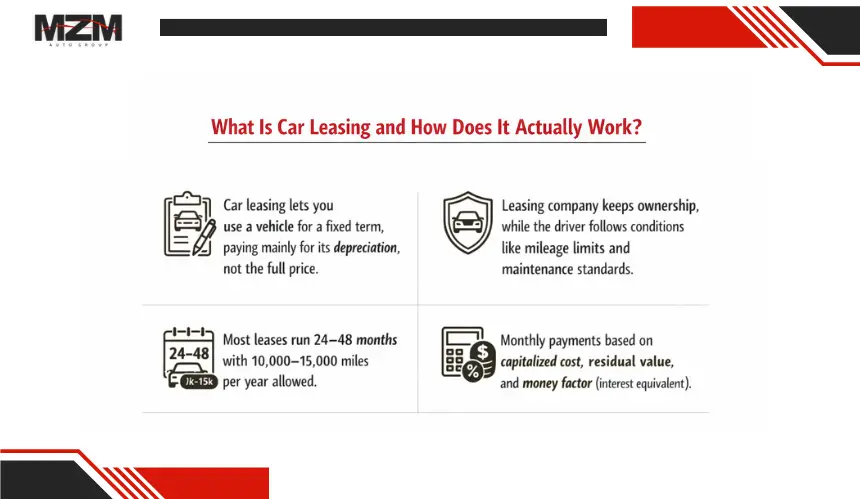

What Is Car Leasing and How Does It Actually Work?

Car leasing is a contractual agreement that allows a driver to use a vehicle for a fixed period while paying primarily for its projected depreciation. Unlike buying, the leasing company retains ownership of the vehicle throughout the term. The driver agrees to specific usage conditions, including mileage limits and maintenance standards, in exchange for lower upfront financial exposure.

At its core, leasing separates vehicle usage from vehicle ownership. You are financing the portion of the car’s value expected to depreciate during your lease term, not the full purchase price.

The Structure of a Lease Agreement

A standard lease typically runs between 24 and 48 months. The contract sets a predefined annual mileage allowance, commonly 10,000 to 15,000 miles per year. Exceeding this limit results in per-mile charges at the end of the term.

Another central component is the residual value, which represents the vehicle’s projected worth at lease maturity. This figure is calculated at the beginning of the agreement and directly affects the depreciation you are responsible for paying.

Because the residual value is predetermined, leasing shifts much of the market depreciation risk to the finance company, but only within the agreed mileage and wear conditions.

Key Financial Components That Shape Your Payment

Lease payments are determined by three primary financial elements:

- The vehicle’s negotiated price (capitalized cost)

- The residual value

- The money factor (the lease equivalent of an interest rate)

The difference between the capitalized cost and residual value represents the depreciation you will pay over the lease term. The money factor adds a financing charge, similar to loan interest. To approximate an equivalent APR, multiply the money factor by 2,400 to get a close estimate.

Unlike loan payments, these payments do not build equity in ownership.

What Happens at the End of the Lease?

When the lease concludes, the driver generally has three structured options: return the vehicle, purchase it for the predetermined residual value, or transition into a new lease agreement.

Early termination is typically expensive because the contract assumes a fixed depreciation schedule. Breaking that schedule often requires paying the remaining balance or substantial penalties.

Did You Know? Key Leasing Insights

New vehicles commonly lose between 20 and 30 percent of their value in the first year alone. This rapid early depreciation is one reason lease payments can appear lower than loan payments.

What Does Buying a Vehicle Mean Financially and Legally?

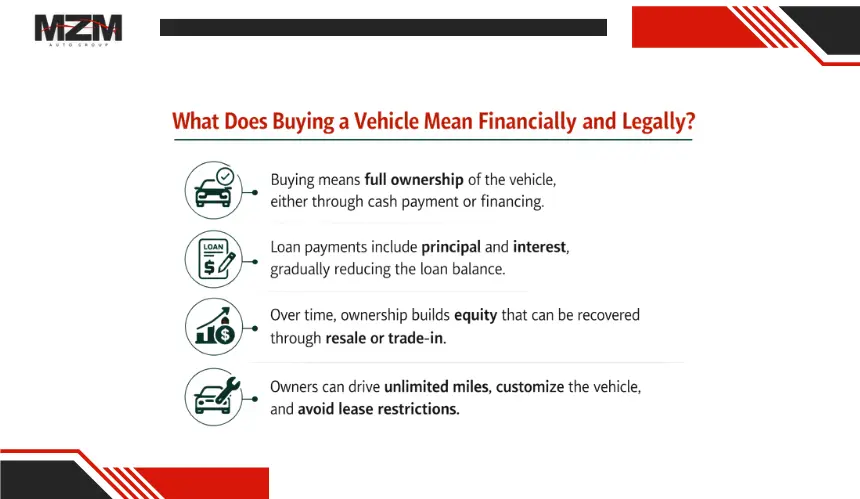

Buying a vehicle changes the entire financial structure of the transaction. Instead of paying for temporary usage, you are acquiring an asset. Whether you pay in cash or finance with an auto loan, the objective is ownership, and ownership carries both long-term advantages and full depreciation exposure.

The key distinction is that every payment made toward a purchased vehicle contributes to eventual equity. Over time, that equity becomes recoverable value through resale, trade-in, or continued use after the loan is paid off.

Buying With Cash vs. Financing

When paying in cash, ownership transfers immediately. There are no monthly obligations, no interest accumulation, and no lender involvement. However, the upfront capital requirement is significantly higher.

Most buyers use financing. In this structure, a lender provides the funds to purchase the vehicle, and the buyer repays the loan over time with interest. Loan terms commonly range from 36 to 72 months, though longer terms have become more common as vehicle prices rise.

An auto loan payment includes both principal (reducing the loan balance) and interest (the cost of borrowing). Over time, a greater portion of each payment goes toward principal reduction.

How Auto Loans Build Equity

Equity is the difference between the vehicle’s market value and the remaining loan balance. In the early months of a loan, depreciation can outpace principal reduction, creating a temporary negative equity position. This is especially common because vehicles often lose 20–30% of their value in the first year.

However, as the loan balance declines, equity gradually builds. Once the loan is paid off, the owner retains the vehicle’s full market value. At that point, the cost structure shifts dramatically because there are no more loan payments, only maintenance and operating expenses.

This “payment-free period” is one of the strongest financial arguments for long-term ownership.

Depreciation and Resale Recovery

Vehicles typically lose 50–60% of their value within five years, depending on brand, mileage, and market demand. While this depreciation reduces asset value, ownership allows partial recovery through resale or trade-in.

Unlike leasing, where the residual value is fixed and ownership never transfers unless a buyout occurs, buying allows the owner to benefit if the used-vehicle market strengthens. During supply shortages in recent years, many owners experienced unusually high resale values, something lessees could not capitalize on unless they exercised a buyout option.

Legal and Structural Advantages of Ownership

Ownership removes contractual mileage restrictions and eliminates lease-end inspection standards. Drivers can customize the vehicle, modify it, or drive unlimited miles without penalty.

There are no disposition fees or excess wear charges. The title ultimately belongs to the owner, making the vehicle a transferable asset rather than a temporary agreement.

Buying shifts depreciation risk entirely to the owner, but it also creates the opportunity for long-term cost stabilization and equity growth.

Next, we will examine the core financial differences between leasing and buying side by side to clarify how these two structures compare over time.

Core Financial Differences Between Leasing and Buying

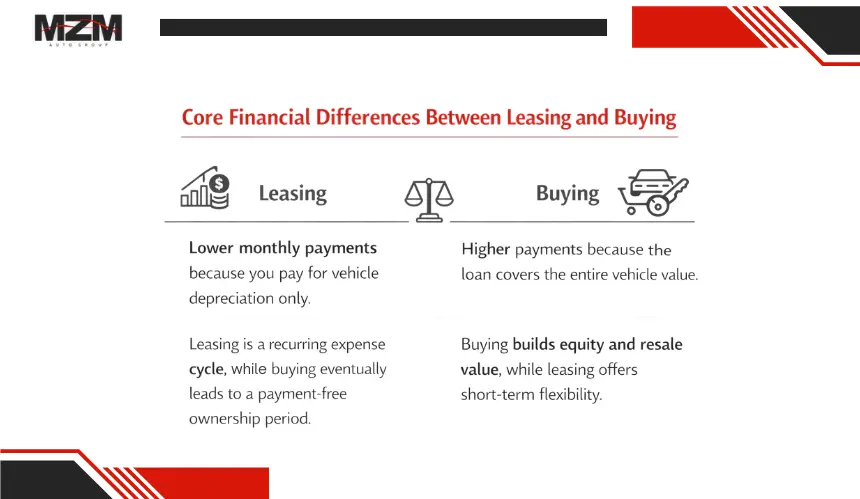

At first glance, leasing often looks more affordable because the monthly payment is lower. But the size of the payment alone does not determine financial efficiency. The deeper comparison involves total lifecycle cost, equity growth, depreciation exposure, and the length of time you plan to keep the vehicle.

Leasing and buying are structured around two different economic models. Leasing prioritizes short-term access and payment predictability. Buying prioritizes long-term asset ownership and eventual cost stabilization.

Monthly Payment Structure

Lease payments are typically lower because you are financing only the vehicle’s projected depreciation during the lease term, not its full purchase price. The calculation is based on the capitalized cost, residual value, lease term, and money factor.

By contrast, an auto loan payment includes both principal repayment and interest on the full vehicle value. That naturally produces higher payments, especially with shorter loan terms.

Note: A very low lease payment can sometimes be driven by a high residual value projection. If the residual is overly optimistic, the leasing company absorbs the risk, but it also means there may be little room for negotiation on the vehicle price.

Did You Know? Multiplying a lease money factor by 2,400 provides a close estimate of the equivalent APR. Many drivers compare lease payments without converting this figure, which can obscure the true financing cost.

Total Cost of Ownership Over Time

Leasing operates on a recurring cycle. After 24 to 48 months, the vehicle is returned, and another lease begins. Over an 8–10-year period, this may result in two or three consecutive payment cycles.

Buying follows a declining obligation model. Once the loan is paid off, often within 5 to 7 years, the owner enters a payment-free period. During those years, the cost of ownership drops significantly because only maintenance, insurance, and operating expenses remain.

Data Insight: Automotive lifecycle studies consistently show that keeping a vehicle beyond loan payoff dramatically lowers average annual cost. The break-even point often occurs around years 6 to 8 of ownership.

Tip: When comparing lease vs buy, divide the total projected out-of-pocket cost by the number of years you expect to drive. This “cost per year” method provides clearer insight than comparing monthly payments alone.

Equity vs Access Model

Leasing does not build ownership equity. At the end of the contract, unless a buyout option is exercised, the driver has no asset to resell or trade.

Buying gradually builds equity as the loan balance declines. Once paid off, the vehicle retains market value. Even if depreciation reduces that value over time, the owner still holds a transferable asset.

Did You Know? Vehicles typically lose 50–60% of their value within five years. However, depreciation slows after year three, which is one reason long-term ownership often becomes more cost-efficient than short lease cycles.

From a financial planning perspective, leasing is categorized as a recurring expense. Buying creates an asset that depreciates but retains some resale value.

Risk Allocation and Market Exposure

Leasing shifts some depreciation risk to the finance company. If the vehicle’s market value drops unexpectedly, the lessee is generally protected, provided mileage and condition standards are met.

Buying exposes the owner to the full impact of resale market fluctuations. If used vehicle values decline, the owner absorbs that loss. If resale values increase, the owner benefits directly.

Market Fact: During supply chain shortages in recent years, used vehicle prices rose dramatically. Owners who purchased vehicles before the spike were able to sell at unusually high prices, while most lessees could only benefit if they exercised their lease buyout option.

Important Note: High annual mileage accelerates depreciation. Drivers exceeding 15,000 miles per year often find leasing less cost-effective due to excess mileage fees and reduced residual flexibility.

Side-by-Side Financial Snapshot

Financial Factor | Leasing | Buying |

Ownership | No | Yes |

Monthly Payment | Usually Lower | Usually Higher |

Equity Accumulation | None | Builds Over Time |

Long-Term Cost | Continuous Cycles | Stabilizes After Payoff |

Depreciation Risk | Partially Shifted | Fully Assumed |

Resale Opportunity | Limited | Full Market Benefit |

The most important takeaway is this: leasing optimizes short-term liquidity and vehicle turnover. Buying optimizes long-term capital efficiency and asset recovery.

The Role of Depreciation in Leasing vs Buying

Depreciation is the financial engine behind both leasing and buying decisions. Every vehicle loses value over time, but the way that loss is distributed, and who absorbs the risk, differs depending on the structure you choose.

In simple terms, leasing pre-packages depreciation into predictable payments, while buying exposes you directly to market-value changes but offers long-term recovery potential.

First-Year Depreciation Shock

New vehicles typically experience the steepest decline in value in the first year.

- Average first-year depreciation: 20–30%

- Value loss in first 3 years: often 40–50%

- Luxury vehicles tend to depreciate faster than mainstream brands

- High-demand trucks and hybrids often retain value better

For buyers:

- Early depreciation can create temporary negative equity

- Loan balances may exceed market value in the first 1–2 years

For lessees:

- This early depreciation is already factored into the lease payment

- The leasing company assumes market risk if values fall below projections

Did You Know? The majority of a lease payment is based on this early depreciation curve. That’s why short lease terms (24–36 months) align closely with peak depreciation periods.

Residual Value: The Core of Lease Pricing

Residual value is the projected worth of the vehicle at lease end. It is expressed as a percentage of MSRP and directly determines the monthly payment size.

- Higher residual value → lower monthly lease payment

- Lower residual value → higher lease payment

- Residual values are set by finance companies, not negotiated

If the vehicle’s actual market value at lease end is higher than the residual value, the lessee may have positive equity in the buyout option.

Tip: Always negotiate the vehicle’s selling price (capitalized cost). Even though residual value is fixed, lowering the capitalized cost reduces the total depreciation you pay.

Depreciation Over Long-Term Ownership

Depreciation slows after year three. This shift significantly affects long-term cost analysis.

For buyers who keep vehicles 8–10 years:

- Loan payments eventually end

- Depreciation spreads across more years

- Cost per mile decreases substantially after payoff

Data Insight: Vehicles retained beyond seven years often deliver the lowest cost per year of ownership due to the payment-free period after loan completion.

This is the tipping point where buying often becomes financially superior to repeated leasing cycles.

Market Volatility and Risk Allocation

Depreciation is influenced by:

- Supply and demand fluctuations

- Fuel prices

- Brand reliability reputation

- Economic cycles

- Technological shifts (e.g., EV adoption)

Leasing partially shields drivers from unexpected resale drops because the residual value is predetermined.

Buying exposes drivers fully to resale fluctuations, but also allows full upside during strong used-car markets.

Market Fact: During recent supply shortages, used vehicle values rose dramatically. Owners benefited directly. Lessees only benefited if they exercised their lease buyout before returning the vehicle.

High Mileage and Accelerated Depreciation

Mileage is one of the strongest drivers of value decline.

- Vehicles driven over 15,000 miles annually depreciate faster

- Lease contracts penalize excess mileage (commonly $0.15–$0.30 per mile)

- High-mileage drivers often experience better flexibility with ownership

Important Note: If your driving patterns are unpredictable, leasing can introduce financial uncertainty due to mileage penalties.

Depreciation cannot be avoided in either model. The difference lies in how it is structured:

- Leasing converts depreciation into predictable short-term payments

- Buying absorbs depreciation upfront but allows long-term value recovery

Next, we’ll examine when leasing makes financial and lifestyle sense, and which types of drivers benefit most from that structure.

When Leasing Makes Financial and Lifestyle Sense

Leasing is most effective when the driver’s habits align with short-term use, predictable mileage, and a preference for lower monthly payments. It is structured for access and flexibility rather than long-term ownership.

Short-Term Vehicle Cycles

Leasing fits drivers who prefer replacing vehicles every 2–4 years. Most leases remain within the manufacturer’s warranty period, which reduces exposure to major repair costs.

Did You Know? The majority of lease terms end before warranty expiration, limiting long-term mechanical risk.

Predictable Cash Flow

Lease payments are typically lower because they cover depreciation rather than the full vehicle value. This can help preserve liquidity and stabilize monthly budgeting.

Tip: Leasing may benefit individuals or businesses prioritizing short-term capital flexibility over equity accumulation.

Controlled Mileage Drivers

Leasing works best when annual mileage stays within contract limits, usually 10,000–15,000 miles per year. Predictable commuting patterns reduce the risk of excess mileage fees.

Technology and Upgrade Preference

Drivers who value regularly upgrading to newer safety systems, EV technology, or infotainment features often prefer leasing. Shorter cycles reduce long-term obsolescence concerns.

Leasing makes the most sense for drivers who prioritize flexibility, warranty coverage, and lower upfront exposure over long-term asset ownership.

When Buying Becomes the Smarter Long-Term Strategy

Buying generally favors drivers with a long time horizon and consistent usage patterns. While monthly payments may be higher at first, ownership creates long-term financial stability once the loan is paid off.

- Long-term cost advantage: After 5–7 years, loan payments end, lowering the average annual cost. Vehicles kept 8–10 years often deliver the lowest cost per year.

- High-mileage flexibility: No mileage caps or excess per-mile charges, making ownership more practical for drivers exceeding 15,000 miles annually.

- Equity building: Each payment reduces principal and builds ownership value. Once paid off, the vehicle retains resale or trade-in value.

- Depreciation slowdown benefit: Value loss slows after year three, improving long-term cost efficiency.

- Full control: No lease-end inspections, customization restrictions, or disposition fees.

Buying becomes financially stronger when the priority is long-term asset retention, mileage flexibility, and cost stabilization rather than short-cycle vehicle upgrades.

Next, we’ll examine hidden costs and contract risks that drivers often overlook in both models.

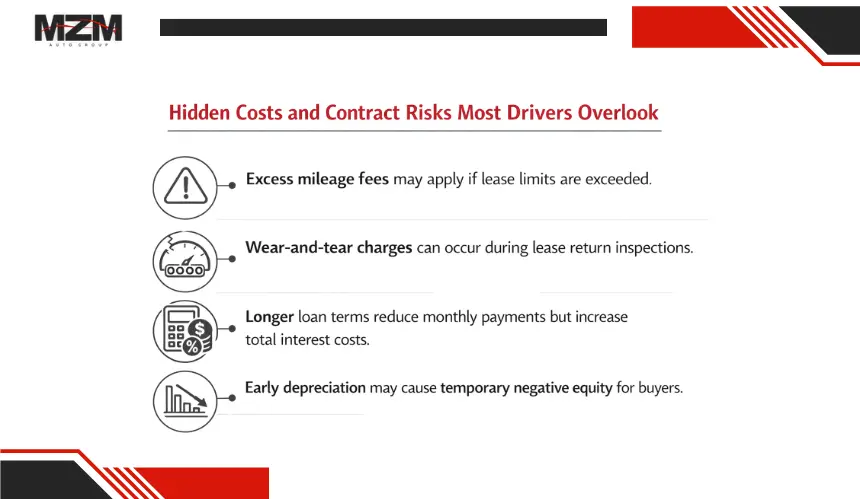

Hidden Costs and Contract Risks Most Drivers Overlook

Monthly payment comparisons rarely tell the full story. Both leasing and buying involve secondary costs that can significantly affect the overall financial outcome if not carefully evaluated.

- Excess mileage charges (leasing): Most leases charge $0.15–$0.30 per mile over the limit. Driving just 3,000 extra miles per year could add hundreds of dollars to the lease end cost.

- Wear-and-tear penalties (leasing): Cosmetic damage, tire condition, and interior wear are assessed during lease-end inspections and may result in additional charges.

- Early termination fees (leasing): Ending a lease early often requires paying remaining depreciation and penalties, which can be costly.

- Interest accumulation (buying): Longer loan terms reduce monthly payments but increase total interest paid over time.

- Negative equity risk (buying): Rapid early depreciation can leave loan balances above the vehicle’s value in the first years.

- Gap insurance requirements: Frequently required for leases and recommended for financed purchases when loan balances exceed market value.

Did You Know? Extending an auto loan from 60 to 72 months can lower the monthly payment but may increase total interest costs by thousands over the life of the loan.

Understanding these hidden variables prevents decisions based solely on monthly affordability and improves long-term financial clarity

Frequently Asked Questions

Is leasing cheaper than buying in the long term?

Leasing often results in lower monthly payments, but the long-term cost depends on how long you keep a vehicle. Over 8–10 years, buying typically becomes more cost-efficient because loan payments end and the vehicle retains resale value. Leasing involves recurring payments without building equity.

Can you negotiate a car lease?

Yes. While the residual value is set by the leasing company, the vehicle’s selling price (capitalized cost) is negotiable. Lowering the capitalized cost reduces total depreciation paid over the lease term. Money factors may also be negotiable depending on credit profile and lender policies.

What happens if you exceed the mileage limit on a lease?

Most lease agreements charge between $0.15 and $0.30 per mile over the contracted limit. For example, exceeding the allowance by 5,000 miles could result in additional charges of several hundred to over a thousand dollars at lease end.

Does leasing affect your credit score differently than buying?

Both leasing and financing appear on your credit report and impact your credit score based on payment history and debt levels. Missed payments harm credit in either structure. Leasing may slightly affect debt-to-income ratios differently because it is structured as a long-term obligation rather than an installment loan.

Can you buy the vehicle after the lease ends?

Most leases include a purchase option at a predetermined residual value. If the vehicle’s market value exceeds the residual price, exercising the buyout may provide a financial advantage. If the market value is lower, returning the vehicle may be the better option.

Is a larger down payment recommended for leasing?

A large down payment reduces monthly payments but does not build equity. Financially, many advisors suggest minimizing upfront cash in leases because the vehicle is not owned, and insurance may not fully recover that upfront amount in a total-loss scenario.

Which option is better for electric vehicles?

Leasing can be attractive for electric vehicles due to rapid advancements in battery technology. It reduces long-term obsolescence risk and uncertainty about resale values. Buying may make more sense if long-term ownership and cost per mile are the priority.